In a new white paper EMAK also highlights fiscal benefits derived from accelerating the transition to electric.

The Electric Mobility Association of Kenya (EMAK) is a diverse and dynamic community that includes industry experts, entrepreneurs, policymakers, academics, innovators, and enthusiastic individuals who believe in the potential of electric mobility to shape a sustainable future. EMAK assumes the role of a strong advocate for electric mobility at all levels, from local communities to national policies. Through engagements with government bodies, regulatory authorities, and relevant stakeholders, EMAK works to create an enabling environment for the growth of electric mobility in Kenya.

EMAK is also dedicated to raising awareness about the benefits of electric mobility through educational programs, workshops, public campaigns, and collaborations with educational institutions. EMAK aims to empower individuals and businesses to make informed decisions and embrace electric mobility solutions. EMAK also actively collaborates with industry players and government agencies to drive the expansion of charging networks, ensuring the accessibility and convenience of charging facilities for EV owners across Kenya. EMAK is also a hub for research and innovation in the electric mobility domain. Therefore, EMAK supports and promotes research projects, technological advancements, and innovative solutions that accelerate the growth of electric mobility while addressing challenges and opportunities unique to our region.

EMAK has just released a new white paper highlighting policy measures and incentives that, if fully implemented, could supercharge Kenya’s electric mobility sector. EMAK says the white paper presents a comprehensive policy and fiscal roadmap for accelerating the adoption of electric vehicles (EVs) in Kenya, positioning the country as a regional leader in clean and sustainable transportation. The paper looks at current market conditions, localization challenges, infrastructure gaps, and evaluates the impact of different levels of government support through scenario modelling from 2025 to 2040.

The paper highlights that across nearly every component required for local manufacturing, local manufacturing costs are at least 50% higher — and in many cases, over 300% higher — than direct imports, despite Kenya’s efforts to support the local assembly sector. The paper lists some of the possible reasons for these high costs of local manufacturing and assembly as:

- Lack of Economies of Scale: Chinese automotive manufacturers for example produce millions of components annually, significantly reducing unit costs through economies of scale. Whereas Kenyan manufacturers operate on a much smaller scale, with limited annual demand volumes that cannot justify large-scale automated production. For example, crash guards and handlebar sets that cost USD 7–10 to import may cost up to USD 70–75 to produce locally due to inefficient tooling and setup costs spread over fewer units.

- High Cost of Raw Materials and Tooling: Kenya lacks a fully integrated supply chain for automotive-grade metals, plastics, and electronic components. Most materials must be imported in smaller quantities, leading to higher per-unit costs. Additionally, the cost of tooling and machinery for precision manufacturing is substantial and often must be amortized over a small production run, significantly inflating the per-unit cost of production.

- High Labour and Energy Costs: Although Kenya’s labour is relatively affordable, local production faces inefficiencies due to limited automation and lower workforce specialization. Furthermore, energy costs in Kenya are among the highest in the region—averaging between KES 20–30 per kWh for industrial consumers—raising operational costs for manufacturers who rely on energy-intensive equipment such as welders, cutters, and CNC machines.

- Regulatory Burdens and Taxes on Inputs: While imported finished products benefit from consolidated import tax calculations, local manufacturers often face multiple layers of taxation: Import Duty on inputs, VAT, Excise Tax, Import Declaration Fees (IDF), and Railway Development Levy (RDL) on raw materials and sub-components. These cumulative taxes inflate production costs and make local manufacturing less competitive.

- Limited Access to Finance and Technical Support: Local manufacturers struggle to access affordable long-term financing for industrial investment, unlike their Chinese counterparts who benefit from state-backed loans and subsidies. In Kenya, high interest rates and lack of dedicated financing schemes for local assembly constrain the sector’s growth and productivity.

- Customs Delays and Logistics Inefficiencies: The time taken to clear raw material consignments at ports, combined with high inland transport costs and infrastructure challenges, adds to the total cost of locally manufactured parts. Conversely, Chinese exports benefit from integrated supply chains and export incentives that minimize delivery times and costs. EMAK says Considering the above disparities, there is a strong policy justification for the Government to introduce targeted tax incentives to level the playing field for local manufacturers. Without such support, local manufacturers will continue to be undercut by imports, leading to deindustrialization and job losses.

EMAK’s paper therefore recommends targeted tax reliefs to enhance local assembly competitiveness and stimulate industrial growth under the “Buy Kenya Build Kenya” policy.

The Proposed Fiscal Measures and Justifications in the white paper are centred on a tiered system of fiscal incentives, including:

- Tax exemptions on VAT, import duty, and excise duty for EVs, batteries, and EVSE.

- Comprehensive incentives under a Special Operating Framework Agreement for large investors (e.g., 0% corporate tax, exempted stamp duty, and customs duties).

These measures aim to:

- Reduce total cost of ownership for EVs.

- Catalyse local value addition.

- Attract foreign direct investment.

- Enable job creation.

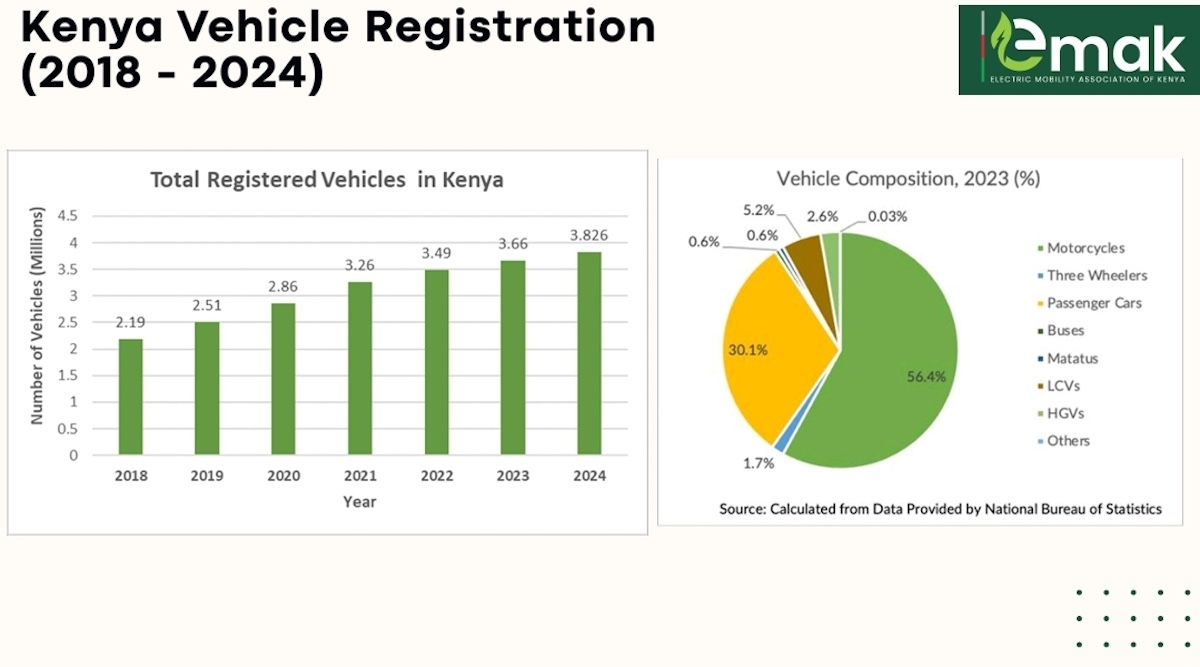

Let’s take a look at Kenya’s current vehicle landscape.

As you can see, motorcycles make up over 50% of the country’s fleet. It’s no surprise then that motorcycles are seeing most of the action in Kenya, and at the moment, the motorcycle sector is the main driver of electric vehicle adoption. In 2024, just over 7% of new motorcycle registrations were electric, followed by 4% for electric tuk tuks, 1.1% for electric buses and minibuses, and then 0.18% for electric cars.

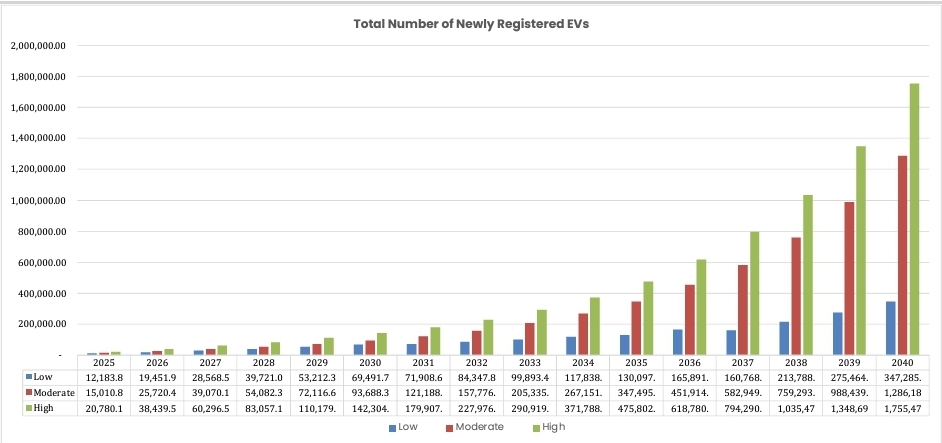

EMAK’s white paper models three adoption scenarios — Low, Moderate, and High Government Support to promote electric mobility:

- Low Support: No subsidies, minimal charging infrastructure, no tax reliefs.

- Moderate Support: Partial tax exemptions, pilot projects, public fleet electrification.

- High Support: Full tax incentives, suitable environments for local assembly and manufacturing, grants for private EV adoption, large-scale infrastructure deployment, and mandatory electrification targets.

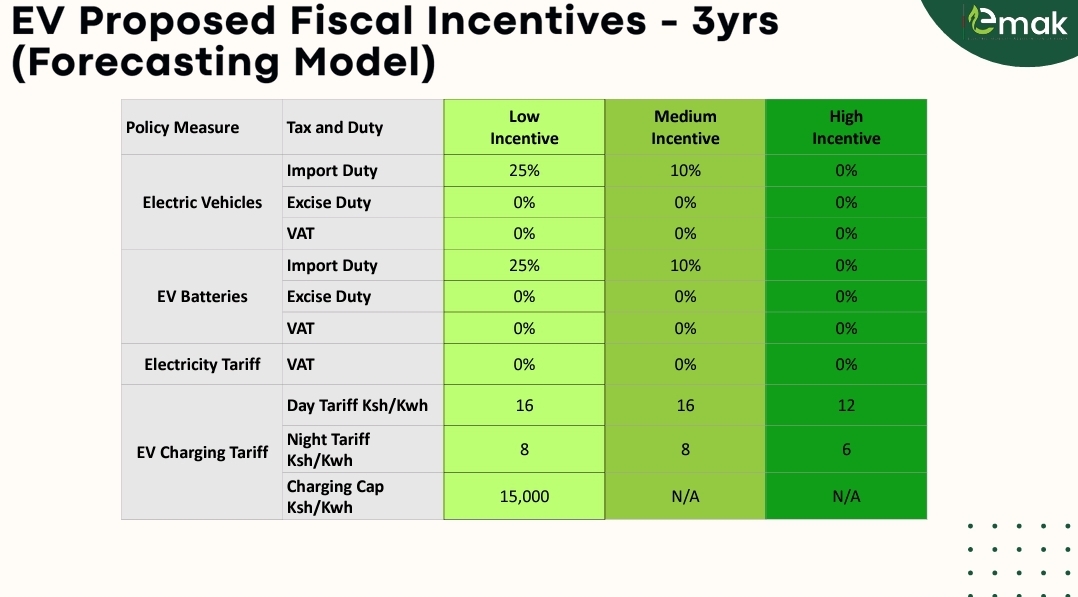

Here is an earlier example from EMAK on the types of interventions illustrated here for a 3-year period.

Results:

- High Support scenario results in over 2 million EVs by 2040, versus 500,000 under a Low Support scenario.

- Electric two-wheelers could reach 1.5 million units by 2040 under High Support, a four times increase over the Low Support scenario.

- The total fuel revenue forgone by 2040 is estimated at USD 1.4 billion, offset by increased electricity sales and EV-related tax revenues.

- CO₂ emissions avoided under the High Support scenario exceed 3.2 million MtCO₂e.

- In all scenarios, growth is driven by the motorcycle sector. For Low Support the number of electric motorcycles grows from 11,097 units in 2025 to 310,718 by 2040. The growth remains modest and suggests that without policy interventions, the electric motorcycle market develops but remains limited in scale and coverage. This is mainly caused by affordability and accessibility of E2W the market. For Moderate Support, the number of electric motorcycles increases from 13,250 units in 2025 to 1,064,620 by 2040, indicating that sustained government support drives rapid market development. High Support, the electric motorcycle stock expands significantly, from 17,552 units in 2025 to 1,506,788 in 2040, demonstrating the impact of cumulative policy impacts and market maturity. By 2040, the stock in the high scenario has more than 4 times the stock compared to the low support scenario. This growth is achieved by the implementation of support mechanisms such as full tax waivers, direct subsidies, suitable electricity charging tariffs, financing schemes, and available charging infrastructure.

Great work from EMAK. Kenya is one of the countries on the African continent that is really trying to promote electric mobility, and most of this is being spearheaded by startups and private companies that are all members of EMAK. It would be great to see more of these associations in more countries on the African continent.

You can find more of EMAK’s current and past work here.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Whether you have solar power or not, please complete our latest solar power survey.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy