Despite its solid position in the first tier of the industry, PowerOak still lags far behind the top three players. The prospectus lays bare a stark reality: the company boasts substantial sales volume but meager profits, remaining in the red for consecutive periods.

Financially, PowerOak’s revenue has grown steadily but shows clear signs of a growth slowdown. It recorded RMB 1.777 billion in revenue in 2023, followed by a 22.4% year-on-year (YoY) increase to RMB 2.174 billion in 2024. However, its revenue for the first three quarters of 2025 stood at only 1.572 billion yuan, with YoY growth plummeting to 3.3%.

The company’s gross margin has kept on rising, climbing from 35.6% in 2023 to 37.3% in 2024, and surging further to 42.3% in the first three quarters of 2025. This figure is well above the 8%-26% gross margin range of B2B energy storage players such as CATL.

Yet the company’s pain point is its failure to translate robust gross margins into stable profitability. Per the prospectus, PowerOak incurred net losses of RMB 184 million in 2023, RMB 46.624 million in 2024 and RMB 29.852 million in the first three quarters of 2025. The core reason for the profit pressure is its substantial investment in sales expenses to expand its overseas market presence. In the first three quarters of 2025, sales expenses totaled RMB 480 million, accounting for 30.5% of its current revenue and continuously eroding its profit margins.

PowerOak’s high gross margins and steep sales costs are both closely linked to its fully integrated DTC (direct-to-consumer) business model. Unlike the industry’s mainstream B2B installer-led model, PowerOak employs a channel strategy of ‘online-first, offline-supplementary’. In the first three quarters of 2025, online channels contributed as much as 71% of its total revenue, with PowerOak reaching end consumers through 45 online stores across 29 third-party e-commerce platforms.

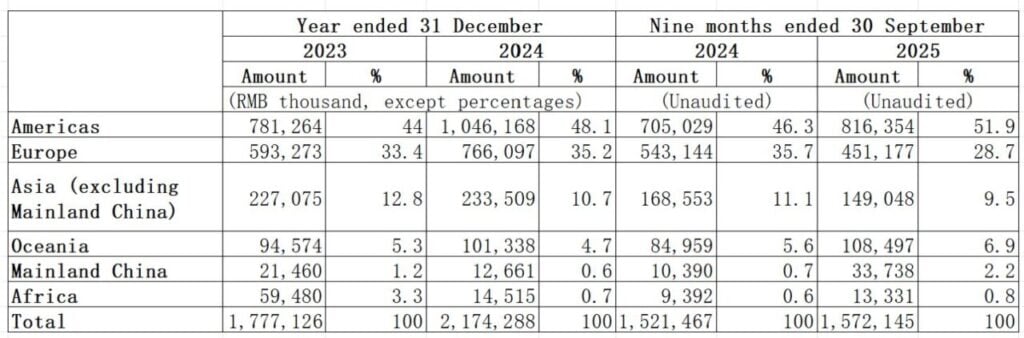

Internationalisation is another defining feature of PowerOak’s business model. Overseas revenue has accounted for over 97% of its total revenue throughout the reporting period, standing at 98.8% in 2023, 99.4% in 2024 and 97.9% in the first three quarters of 2025. Europe and the Americas are its primary markets, making up 48.1% and 35.2% of its 2024 revenue respectively.

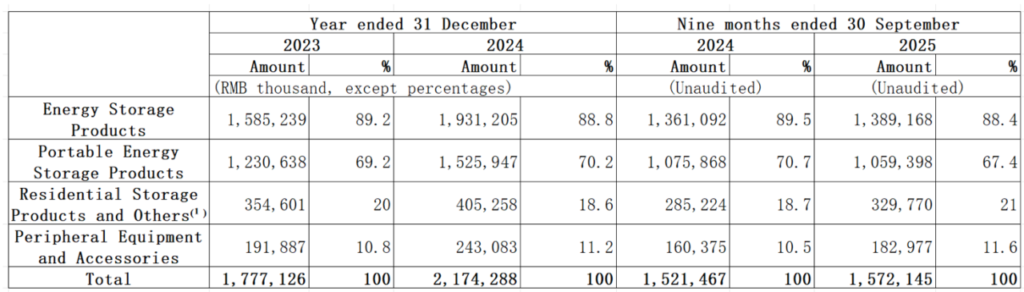

In the first three quarters of 2025, PowerOak’s portable energy storage revenue fell slightly by 1.5% YoY, signaling that growth in this single product category has hit a ceiling. To break through this growth bottleneck, PowerOak has launched multi-dimensional expansion initiatives, including entering industrial, commercial, and residential storage sectors, and developing its ES series products tailored for small and medium-sized enterprises, in a bid to establish its ‘second growth curve’.

PowerOak’s push for a Hong Kong listing is driven by three core objectives: to replenish cash flow through equity financing, alleviate ongoing profit pressure, and secure sufficient capital for future market expansion initiatives.