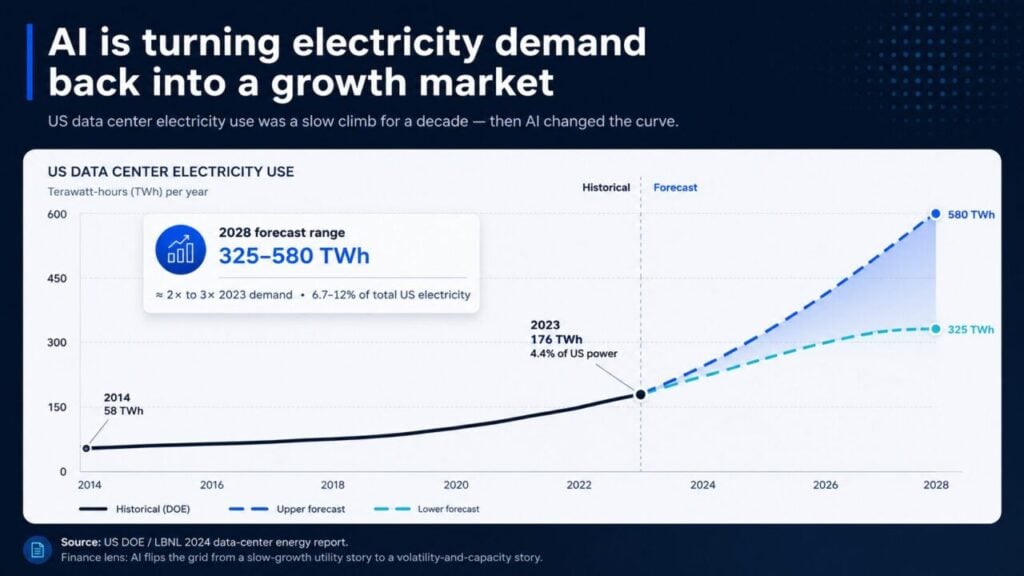

The result is that electricity is once again becoming a growth market.

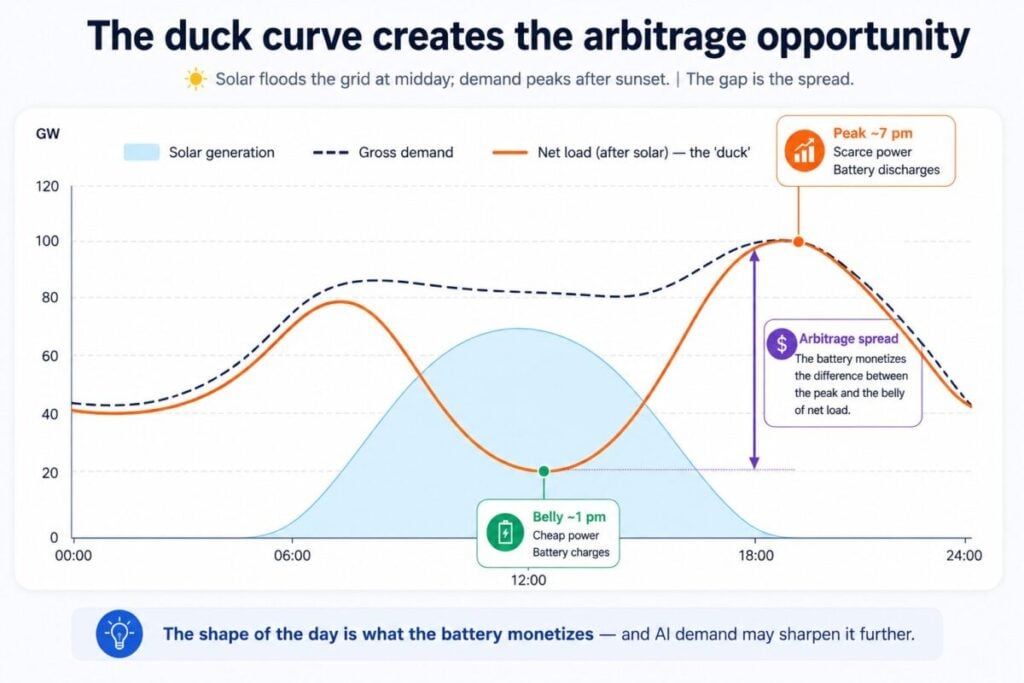

At the same time, the supply side of the grid is also changing rapidly. Renewable generation, especially solar, now represents a growing share of electricity production. Solar power is inexpensive and abundant during midday hours, but production falls sharply after sunset, even as residential and commercial demand remains elevated. This creates widening intraday imbalances between when electricity is generated and when it is actually needed.

Battery storage as the flexibility layer

This changing load profile is one reason modern electricity markets increasingly require flexibility rather than simply more generation capacity. The grid now needs assets capable of absorbing excess energy during periods of oversupply and releasing it rapidly during scarcity events.

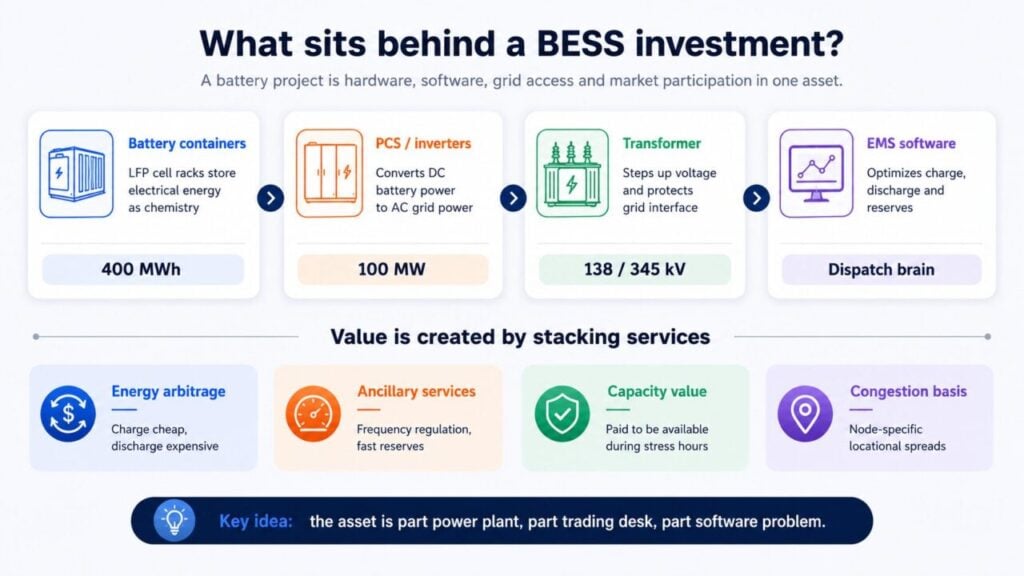

A utility-scale BESS is effectively a large rechargeable battery connected directly to the electricity grid. A typical project might be rated at 100MW/400MWh, meaning it can discharge 100 MW continuously for 4 hours.

Utility-scale lithium-ion systems that cost more than US$1,200/kWh installed roughly a decade ago have, in some markets, fallen below US$300/kWh, materially changing deployment economics and accelerating storage adoption globally.

A BESS combines electrochemistry, power electronics, grid interconnection infrastructure and software-driven dispatch optimisation into a single asset.

Revenue stacking and the ‘Duck Curve’

The physical system includes battery containers that store electricity chemically, inverters that convert DC battery power into AC grid power, transformers that connect the facility to transmission infrastructure, and an energy management system (EMS) that functions as the operational brain of the asset.

But batteries do not generate value from hardware alone. Their economics emerge from market participation.

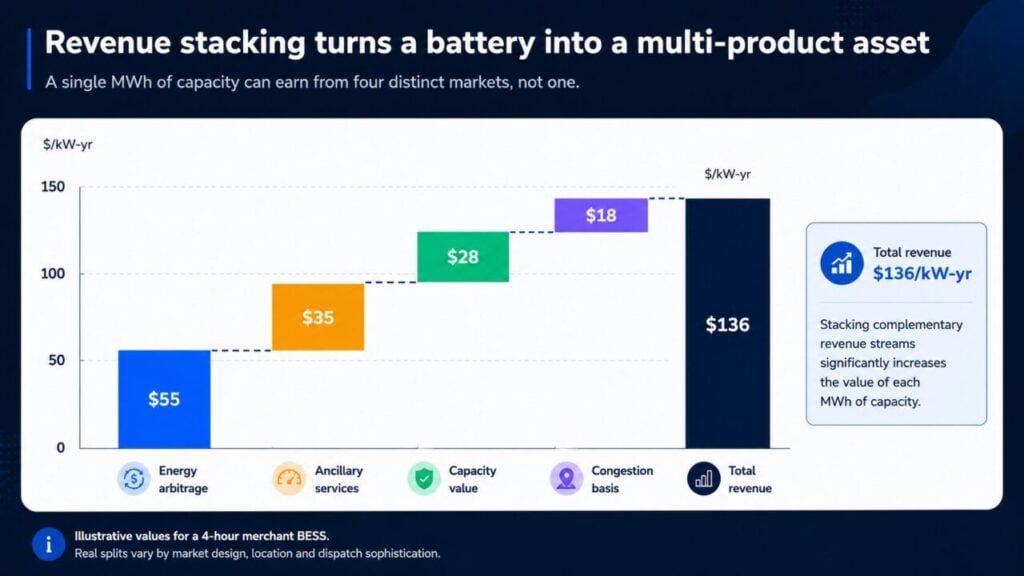

A BESS can simultaneously participate in several distinct revenue streams, including energy arbitrage, ancillary services, capacity markets and congestion pricing.

In the Great Britain (GB) and ERCOT, Texas, merchant markets, battery revenues briefly exceeded £150,000 (US$198,000) to £200,000 per MW per year during periods of elevated volatility, before revenue compression emerged as storage penetration increased.

The key point is that a battery is not a single product infrastructure asset. It behaves more like a multi-strategy trading platform attached to a physical machine.

The battery earns money precisely because the grid is imbalanced.

As solar generation increases during midday hours, net electricity demand on the grid falls sharply because solar offsets conventional generation requirements. After sunset, solar output collapses while demand remains high, creating a steep evening ramp in net load. The resulting shape resembles a duck: a low midday ‘belly’ followed by a sharp evening ‘neck.’

At midday, solar floods the grid with inexpensive electricity, often depressing prices dramatically. Batteries charge during these hours. In the evening, when solar disappears and demand peaks, electricity becomes scarce and prices rise sharply. Batteries discharge into that scarcity.

The economic spread between the midday belly and evening peak is the revenue opportunity.

Why BESS behaves like a portfolio of options

Importantly, batteries do not simply respond mechanically to prices. Operators continuously make optimisation decisions under uncertainty. They must decide whether to charge now or wait, discharge immediately or preserve energy for later, participate in ancillary service markets instead of energy markets, preserve battery cycle life rather than pursue marginal revenue, or hold capacity in reserve for scarcity events.

Most lithium-ion systems are currently economically optimised around roughly 6,000 to 10,000 equivalent full cycles, making degradation modelling central to long-term valuation.

This operational flexibility means a battery behaves economically less like a conventional infrastructure asset and more like a portfolio of embedded real options.

The real options problem behind BESS deployment

The challenge extends beyond battery dispatch. It also applies to the investment decision itself.

In classical infrastructure finance, projects are often evaluated using discounted cash flow models that assume investment occurs immediately once expected returns exceed the cost of capital. But this logic becomes incomplete when investments are irreversible and future market conditions remain highly uncertain.

This was the central insight of the real options framework developed by economists Avinash Dixit and Robert Pindyck in their landmark 1994 work Investment Under Uncertainty (Princeton University Press). Their framework showed that under uncertainty, the ability to delay an irreversible investment has economic value in itself.

That framework maps naturally onto modern battery storage markets.

A utility-scale BESS requires large upfront capital expenditures, faces uncertain future revenues, and operates in rapidly evolving electricity markets shaped by AI demand growth, renewable penetration, regulatory redesign and transmission congestion. Once deployed, much of the capital is effectively irreversible.

As a result, developers are not simply valuing the battery asset. They are also valuing the timing option surrounding deployment itself.

Waiting may create value if battery costs continue to decline, ancillary service markets become saturated, interconnection queues improve, AI-driven demand growth accelerates scarcity pricing, or market rules evolve in favour of storage operators.

Conversely, delaying too long may forfeit advantageous queue positions, land access, tax incentives or early scarcity rents.

The investment decision, therefore, resembles an American-style real option in which the owner continuously evaluates whether immediate deployment or delayed commitment maximises long-term value under uncertainty.

In this sense, BESS projects are not merely flexible operating assets. They are also flexible capital allocation decisions embedded inside a rapidly evolving power system.

The cannibalisation problem

One of the central risks in battery storage markets is cannibalisation.

As more batteries enter a market, they increasingly compete against one another for the same volatility spreads and ancillary service revenues. The very success of battery deployment can compress the economics that originally justified deployment.

This dynamic has already appeared in several mature storage markets. In Great Britain, revenues from Dynamic Containment and other frequency response products fell sharply after rapid storage buildout increased competition among operators. Similar patterns emerged in parts of the California ISO (CAISO) market as battery penetration accelerated.

Cannibalisation matters because it directly affects the option value of waiting described in the Dixit and Pindyck framework.

If developers expect future battery revenues to decline as competitors deploy additional capacity, the incentive may shift toward earlier deployment in order to capture scarcity rents before markets saturate. However, if operators instead expect battery costs to continue falling faster than revenues compress, delaying investment may still maximise value.

In other words, the economics of a battery project depend not only on future electricity markets, but also on expectations about how quickly competing developers exercise their own deployment options.

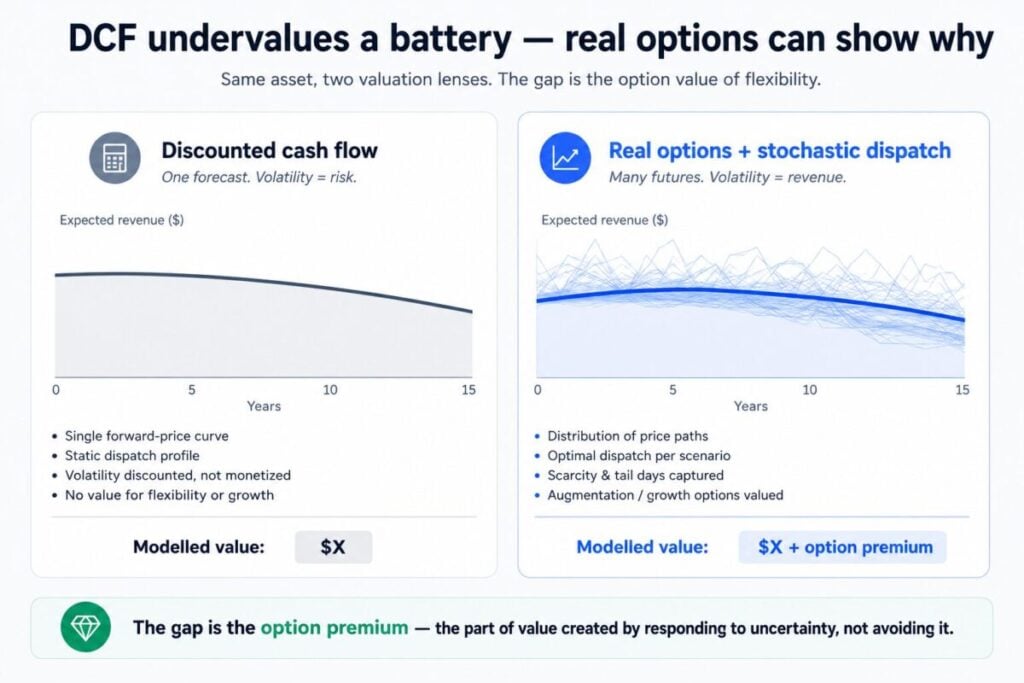

Why DCF models often fail

Traditional discounted cash flow (DCF) frameworks are often poorly suited for merchant battery assets because standard DCF approaches assume relatively static operating behaviour and deterministic revenue forecasts.

Conventional DCF frameworks struggle not only with dispatch volatility, but also with the option value of delaying irreversible battery investments under uncertainty.

In many conventional infrastructure projects, volatility is treated primarily as a risk factor that increases discount rates. For a battery, volatility is also a source of revenue.

The wrong modelling framework can therefore materially undervalue a BESS project.

The modelling challenge

A more realistic framework instead models multiple future price paths, stochastic dispatch optimisation, scarcity events, dynamic operational decisions and future augmentation choices.

In effect, the battery’s value emerges not only from expected average prices but from the distribution of possible market conditions and the operator’s ability to adapt dynamically.

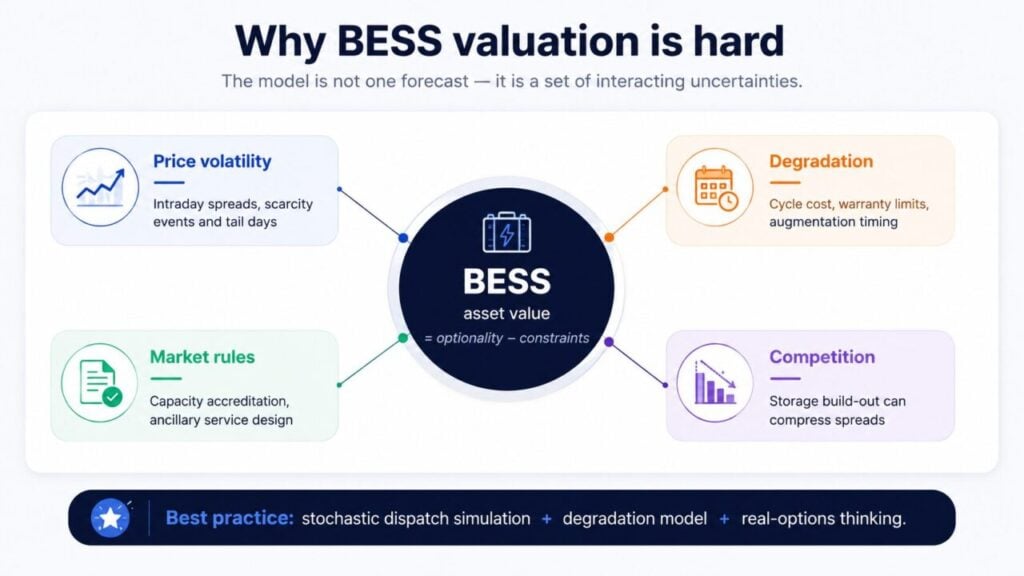

This makes BESS one of the most challenging infrastructure assets to model quantitatively. Analysts must forecast not just electricity prices, but also renewable penetration, transmission congestion, ancillary service saturation, battery degradation, regulatory rule changes, AI-driven demand growth and competition from future storage deployments.

All of these variables interact with one another.

Conclusion

Battery storage is not simply another renewable energy asset. It represents a deeper transition in how electricity systems operate and how infrastructure itself is valued.

In the AI-augmented grid, flexibility has become monetisable. Volatility has become investable. Operational adaptability increasingly matters as much as physical ownership.

For finance professionals, the lesson is clear: valuing a battery increasingly requires combining traditional infrastructure finance with stochastic optimisation and real options analysis.

The future grid may ultimately reward not the assets that produce the most energy, but the assets that respond most intelligently to instability itself.

Selected references

Dixit, A. & Pindyck, R. (1994). Investment Under Uncertainty. Princeton University Press.

California ISO (CAISO) battery storage market reports.

NESO and National Grid ESO Dynamic Containment market publications.

Modo Energy and LCP Delta battery revenue analytics.

About the Author

Partha Sharma is President of BBNR Capital Management, where he focuses on energy infrastructure valuation and the application of quantitative methods to energy markets. An engineer by training with more than 20 years of experience in the energy industry, he founded BBNR in 2018 after transitioning into finance. He holds an MSc in Global Finance and Banking from King’s College London and a postgraduate certificate in Artificial Intelligence and Machine Learning from The University of Texas at Austin.